You’re Earning $250K+, So Why Aren't You Accumulating Real Wealth?

Run your own numbers. Quantify the drag.

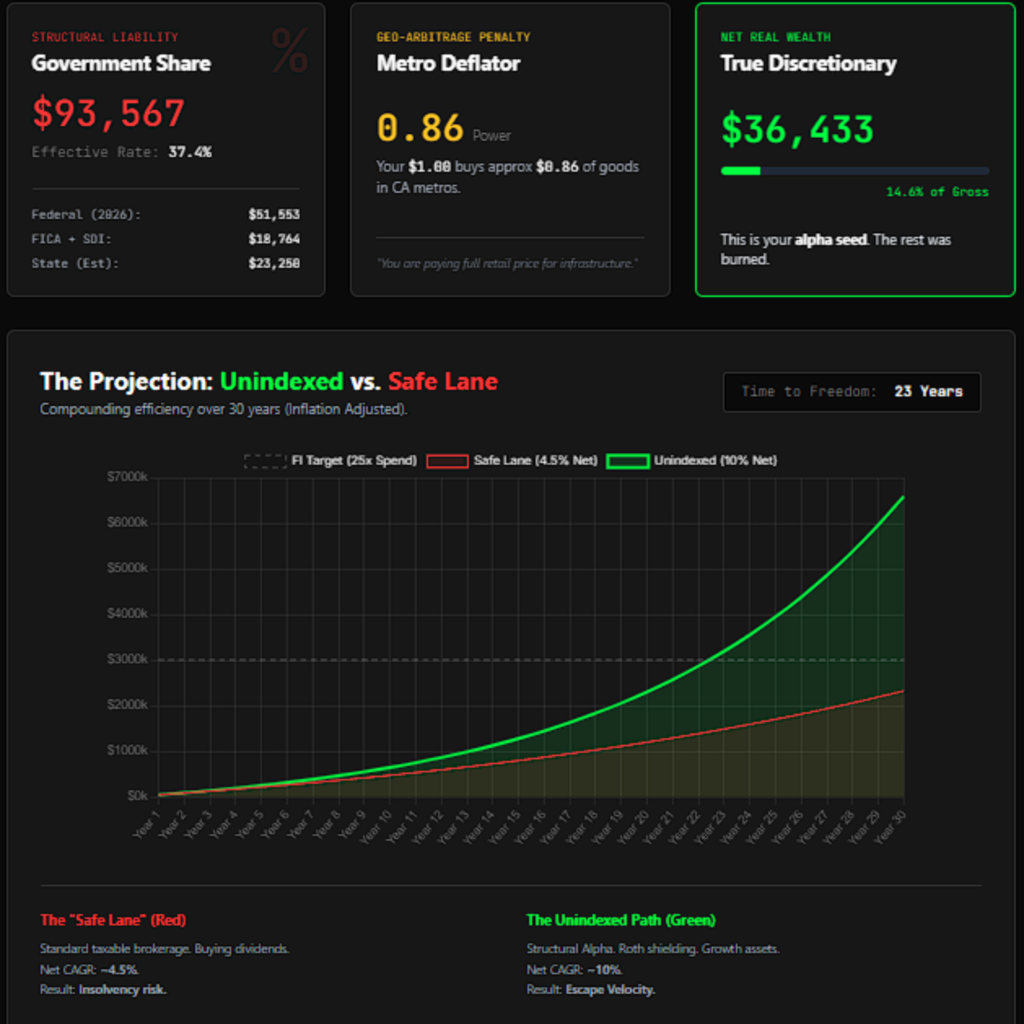

Living in a high-cost-of-living city on a high salary often feels like running on a treadmill. Between aggressive tax brackets, inflated housing costs, and the baseline expenses of just existing, your massive top-line income is being quietly liquidated before you can even invest it. We call this Structural Bleed.

Stop guessing where your money is vanishing. Download the Unindexed Real Wealth Auditor to map out exactly how taxes and HCOL realities are draining your wealth—and discover the exact moves you need to make to plug the leak and start building actual, real wealth.

We’ll email the Auditor directly to your inbox.